Cross-border payouts

Streamlining Global Financial Transactions

International Payouts and Cross-Border Payments

International Payouts and Cross-Border Payments refer to the seamless transfer of funds from a sender's account to a recipient in another country. These transactions enable individuals and businesses to conduct cross-border financial activities efficiently and securely.

Who is it for?

Our International Payouts and Cross-Border Payments solution is designed to cater to a wide range of stakeholders:

Business Users

- Corporations looking to automate global accounts payable, including payments to vendors/suppliers, freelancers, and marketplace purchases.

- Corporates with global offices, transferring payments for business operations, managing payroll, and reimbursements.

Individual Users

- Remittance by expats and migrants to friends and family in their home country.

- Purchase expenses - marketplace purchases, imported goods, stock investments, logistics, travel bookings, and many more.

Why Choose Our International Payouts and Cross-Border Payments Solution?

- Global Payments Made Easy: Say goodbye to the hassles, delays, and exorbitant fees associated with traditional banking. Our solution enables you to make global payments to anyone, whether it's an individual or a corporation, without the complexities.

- Expanded Geographical Reach: Expand your business's reach to new geographies with confidence. Our solution supports transfers to 42 countries and is rapidly expanding, ensuring you can connect with customers and partners worldwide.

- Competitive Real-Time FX Rates: Enjoy competitive foreign exchange (FX) rates in real-time for currency conversions. Our transparent fee structure ensures you get the best value for your money.

- Efficient Currency Management: Mitigate currency risk and optimize your financial operations. Take advantage of our quote blocking feature, which allows you to lock in exchange rates for a defined period without requiring recipient information or funds.

- Monetization Opportunities: Maximize revenue potential by setting up markups and discounts on fees and foreign exchange rates. Our solution empowers you to generate additional income streams from your cross-border payment offerings.

- Faster Transactions: Experience fast and efficient transaction processing. Most fund transfers arrive on the same day, ranging from instant to T1 day, ensuring your payments are delivered promptly (except for the USA).

- Superior User Experience: Our user-friendly APIs and seamless transaction fulfillment process ensure a smooth and intuitive experience for both you and your customers. Real-time webhooks enable you to track transaction status and provide timely updates.

- Regulatory Compliance and Security: Transfer funds globally with confidence. Our solution adheres to strict regulatory compliance and security standards, ensuring the safety and privacy of your transactions.

- Enhanced Client Servicing: Access comprehensive information and reports through our intuitive one-stop portal, AdminNet. Track corridors, recipients, and transaction details conveniently, enabling you to deliver exceptional client servicing and support.

- Auto Reconciliation: Say goodbye to the complexities of handling forex and payment reconciliation manually. Our solution automates these processes, saving you time and reducing errors.

How does it work?

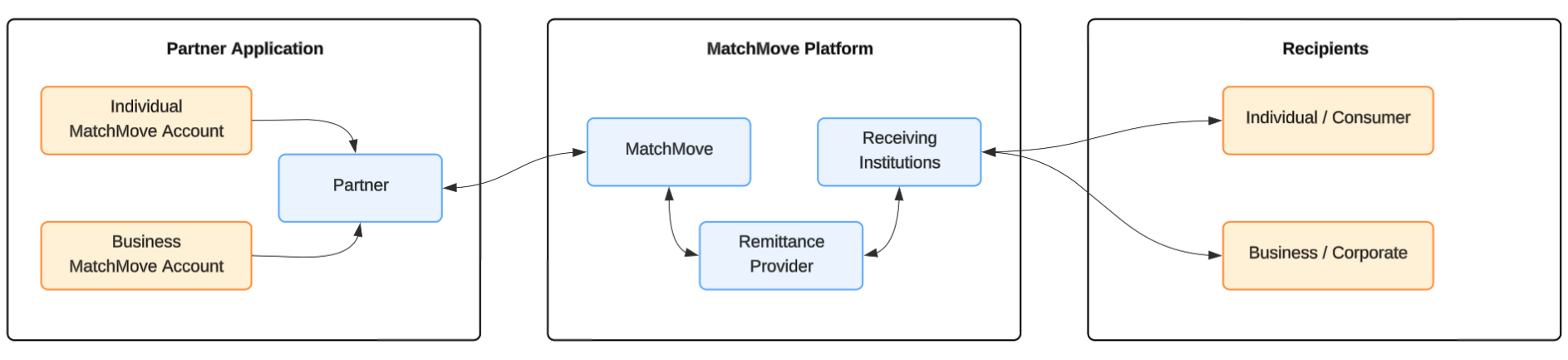

Typical Cross-border Payments workflow

The International Payouts and Cross-Border Payments process involves various participants working together seamlessly:

- Partner Application: Our valued clients integrate our platform into their applications, offering our solutions to their end customers.

- MatchMove Issued Accounts: Individual and corporate accounts issued by MatchMove, representing the senders in the payment flow.

- MatchMove: The MatchMove platform offers a comprehensive solution for seamless fund transfers. We ensure the secure passage of funds from the sender to the recipient.

- Provider: Intermediary parties that MatchMove connects with to provide maximum coverage. We collaborate with trusted providers to ensure global reach and accessibility.

- Receiving Institutions: The financial institution or entity on the recipient side that has a service relationship with the recipient. This can include banks, mobile wallet providers, or other supported account types in local jurisdictions.

- Recipient: The individual or corporate entity receiving the funds from the sender. They can be located in any country supported by our solution.

Remittance Route

An active remittance route should be available before we can initiate a remittance transaction. The enabled routes are configured at the program level as outlined in the contract. Though a remittance route is enabled, it needs to be on available and in an active status to be usable.

Several factors can affect a remittance route:

1. Recipient Country

The receiving country or region of the cross-border payment.

2. Recipient Institution Type

The termination point or the receiving institution of the remittance. e.g., banks, mobile wallets, etc.

2. Remittance Modes

The sender type and the recipient type determine the mode of remittance. The list of enabled remittance modes activated for a program is dependent on the contract and program configuration.

B2B remittance mode

The sender account type is a Business (Corporate), and the recipient account type is also a Business (Corporate).

B2C remittance mode

The sender account type is a Business (Corporate), and the recipient account type is a Consumer (Individual).

C2B remittance mode

The sender account type is a Consumer (Individual), and the recipient account type is a Business (Corporate).

C2C remittance mode

The sender account type is a Consumer (Individual), and the recipient account type is a Consumer (Individual).

3. Remittance Rails

Each corridor will have an option on which remittance rail the transaction will be processed on.

LOCAL

Remittances will be processed using the local transfer networks available in the receiving country.

Maximum per transaction limit:

- Varies depending on the corridor and remittance mode.

Maximum transacition velocity per N days:

- Varies depending on the corridor limit.

Delivery timeline:

- 30 minutes to T+1 as long as transactions are initiated within the cut-off time.

- Cut-off time is dependent on the corridor setting.

Quote expiry:

- 30 minutes to 1 hour

Sender name in the transaction:

- The

Sender namesent as part of sender remarks when the transaction is sent will be forwarded to the receiving partner by Matchmove. However, it depends on the receiving institution to display the Sender name in the recipient transaction statements.

SWIFT

Remittances will be processed using the SWIFT rail from the sender country to the receiving country.

Maximum per transaction limit:

- Normally, transactions can go as high as

up to 1 million USD. - For transaction value greater than the review threshold amount*, a supplementary document (such as invoices) is mandatory to be uploaded.

- While, transactions

exceeding 1 Million USD, will need to undergo a pre-approval process where additional documents will be solicited offline and approval must be given prior to the initiation of the transaction.

*review threshold amount — is a product internal threshold that is set based on risk and may change without notice.

Maximum transaction velocity per N days:

- Varies depending on the corridor limit.

Delivery timeline:

- T+1 as long as transactions are initiated within the cut-off time.

- Cut-off time: 4:30 PM SGT on the working days excluding bank holidays.

Quote expiry:

- Same currency transfer - up to 10 hours

- Cross currency transfer - 5 mins

Sender name in the transaction:

- SWIFT will be using the payments-on-behalf-of (POBO) model. Where transactions are processed by a third-party service (

Payment Rail Provider) on behalf of a business and individual senders. As such, the sender name that will be in the transaction and recipient bank statement is the Payment Rail Provider name, and not the sender details. The MT103 files will also contain the same details irrespective of what information is sent in transactionremarks.

The enablement of the remittance routes is based on the enabled routes in the program configuration. This program configuration aligns with the capabilities and features outlined in the contract.

- Route example 1: (SGP to USA, B2B, Bank, via SWIFT), where the remittance corridor is open for transfer from Singapore to the USA, for Business (sender) to Business (recipient), the receiving institution can be a bank, and the remittance will be processed via the SWIFT network.

- Route example 2: (SGP to USA, B2B, Bank, via LOCAL), where the remittance corridor is open for transfer from Singapore to the USA, for Business (sender) to Business (recipient), the receiving institution can be a bank, and the remittance will be processed using LOCAL transfer networks available in the receiving region.

The availability of the remittance routes can be affected by maintenance schedules on the remittance rail. So it is important to check whether a certain remittance route is active before a remittance transaction is attempted.

Components of a Cross-border Payout

Successfully sending a cross-border payout or international remittance requires two key components.

Remittance Recipient

A recipient entity must be defined according to the remittance form requirements of a selected Remittance Route. The remittance form requirements should include the address, bank account details, and other key information required by the regulatory body of the recipient region.

The recipient details defined in the recipient profile will be used for risk evaluation. A recipient can only be used for a remittance transaction if its status is active.

Remittance Quotation

A remittance quotation is a snapshot of the rate and computation of the charges that will be applied to send a particular remittance transaction. A quotation can be generated by providing the intended amount to be remitted and the remittance route details. A quotation can be used for a remittance transaction as long as it is valid and unexpired.

1. Remittance Recipient

The platform can send remittance transactions to two types of receiving entities:

Individual recipient (Consumer)

Consumer information from the individual will be gathered to ensure compliance with the remittance regulatory standards of the receiving country.

Business recipient (Corporate)

Corporate information from the business will be gathered to ensure compliance with the remittance regulatory standards of the receiving country.

Recipient Creation Methods

A remittance recipient, regardless of type, can be defined in two ways:

- Pre-transaction creation - creating a remittance recipient before the actual sending of the remittance transaction.

- In-transaction creation - creating a remittance recipient alongside the sending of the remittance transaction.

When a new remittance recipient is created, it will go through a series of stages before becoming active and ready to use.

Recipient Status

Only when a remittance recipient is on the active state, will it be allowed to be used for sending a remittance transaction.

CREATED | The initial state right after the recipient creation |

PENDING | The risk evaluation is in progress and/or the recipient is in a cooling period state. |

ACTIVE | The recipient is cleared for risk, and the sending of remittance is enabled |

BLOCKED | The recipient is permanently disabled due to the risk. This state is permanent and irreversible |

DELETED | The recipient is removed from the user's recipient list. This state is permanent and irreversible |

INACTIVE | The recipient is temporarily disabled. The state is reversible by reactivation |

UPDATE_REQUIRED | The recipient needs to be updated, because the recipient form fields were updated |

FAILED | The recipient creation failed due to a system error. |

DEACTIVATED | Deprecated as of May 2025 and is replaced by the INACTIVE status. |

PENDING_REVIEW | Deprecated as of May 2025 and is replaced by the PENDING status. |

Recipient Cooling-Off Period

A cooling-off period is a mandatory waiting timeframe imposed on payout recipients during which certain account functionalities, such as withdrawals or transfers, are temporarily restricted. This regulatory safeguard is designed to prevent system abuse by slowing down the velocity of movement, providing a "buffer" to detect and intercept fraudulent activity or unauthorized access. By disabling specific recipient interactions during this window, financial systems can ensure that high-risk actions are verified and intentional before the funds or services become fully accessible again.

In MatcMove, the cooling period is effective between recipient creation to activation. It serves as a fraud prevention measure, providing a buffer window during which suspicious activity can be detected before the recipient becomes eligible for payouts.

The cooling period starts immediately upon recipient creation and runs in parallel with the risk evaluation. Neither process waits for the other — both must independently complete before the recipient can become ACTIVE.

2. Remittance Quotation

When a remittance quotation is generated, the rates and fees will be locked and reserved for a certain period of time.

During this time, the quotation can be used for a remittance transaction with the locked computed rates and fees.

A quotation will be marked with an expiry timestamp, e.g. "expiry": "2024-04-04T16:31:01 +08:00", indicating the period on until when it can be used.

Also, a quotation and quotation ID can only be used by one remittance transaction. When a quotation is consumed or expired, a fresh quotation must be generated for the transaction.

Quotation Modifiers

In addition to the intended amount to be remitted and the remittance route details, a few additional modifier fields may be required:

FORWARD quotation | User inputs the sender amount in the sender's currency. Then the recipient amount will be calculated. | Fee Included | The sender has a fixed amount to be sent (budget), and the fee needs to be included in that amount. e.g., Remittance to families in a home country. | The fees will be deducted from the Sender amount (Sender amount - fees), which will decrease the Recipient amount (Converted Sender amount - fees). While the Sender deductible (wallet debit) will remain unchanged (Sender amount). |

Fee excluded | The sender wants to convert the amount to be sent and pay for the additional fees the remittance will incur. e.g., Employee salary, freelancer payments, bill payments in a different currency | The fees will not be deducted from the Sender amount (Sender amount), and the Recipient amount will remain intact (Converted Sender amount) While the Sender deductible (wallet debit) will be added with fees (Sender amount + Fees) | ||

REVERSE quotation | User inputs the recipient amount in the recipient's currency. Then the sender's deductible amount will be calculated. | Fee excluded | User wants to send a fixed amount in the recipient's currency to the recipient. e.g., Marketplace payments, invoice payments for goods purchased in the destination country. | The fees will not be deducted from the *Derived Sender amount (Derived Sender amount), and the Recipient amount will remain intact (Converted Sender amount) While the Sender deductible (wallet debit) will be added with fees (Sender amount + Fees) *Derived sender amount = Recipient amount / FX rate |

Related Links

On this page

- Cross-border payouts